It’s Time to Unbundle ESG

It’s Time to Unbundle ESG

ESG is at an inflection point. It has come to represent a broad and inchoate aspiration for what business should be doing beyond maximizing shareholder value.

In the summer of 2023, a prominent business trend seemed to reach a dramatic and an unexpected end. Larry Fink, the CEO of BlackRock, the world’s largest asset manager with more than $9 trillion under management at the time, announced that he would no longer use the term “ESG” to describe the company’s approach to investing. While interest in environmental, social, and governance (ESG) performance has grown over the last two decades, an accelerating backlash in the U.S. against “woke” investing delivered what looks like a fatal blow.

BlackRock has long been seen, by virtue of its size and Fink’s outsized megaphone, to be the trendsetter when it comes to the future of business. If it was abandoning ESG, has the movement run its course? Have we reached “peak ESG”?

As business school professors we’ve long studied the relationship between business and society — including when some of today’s ESG topics were referred to as corporate social responsibility (CSR), corporate sustainability, and socially responsible investing (SRI).

The origin story is, perhaps fittingly, a tale of demand and supply. Demand arose from corporate investors, including pension funds and other institutions and individuals seeking to either avoid stocks of companies that heavily externalized to society some of their costs (think heavy polluters) or product consequences (think smoking and handguns), or to pressure such companies through shareholder proposals and other tactics to encourage them to change their ways. On the supply side, there were companies doing the work to measure, disclose, and improve ESG issues like carbon emissions, product safety, and corporate governance. In between there emerged a set of financial intermediaries offering and using ESG ratings and due diligence to match demand and supply.

While there is a long history of individuals, communities, churches, nonprofits, and governments pressuring business to adhere to societal expectations, the movement really took off in the early 2000s, bolstered by the influential 2004 United Nations “Who Cares Wins” report. The ESG movement coalesced around the idea that by managing environmental, social, and governance factors that were material to the business — that is, those relevant to a company’s competitiveness and reputation that could affect stock prices — corporate leaders could increase financial performance.

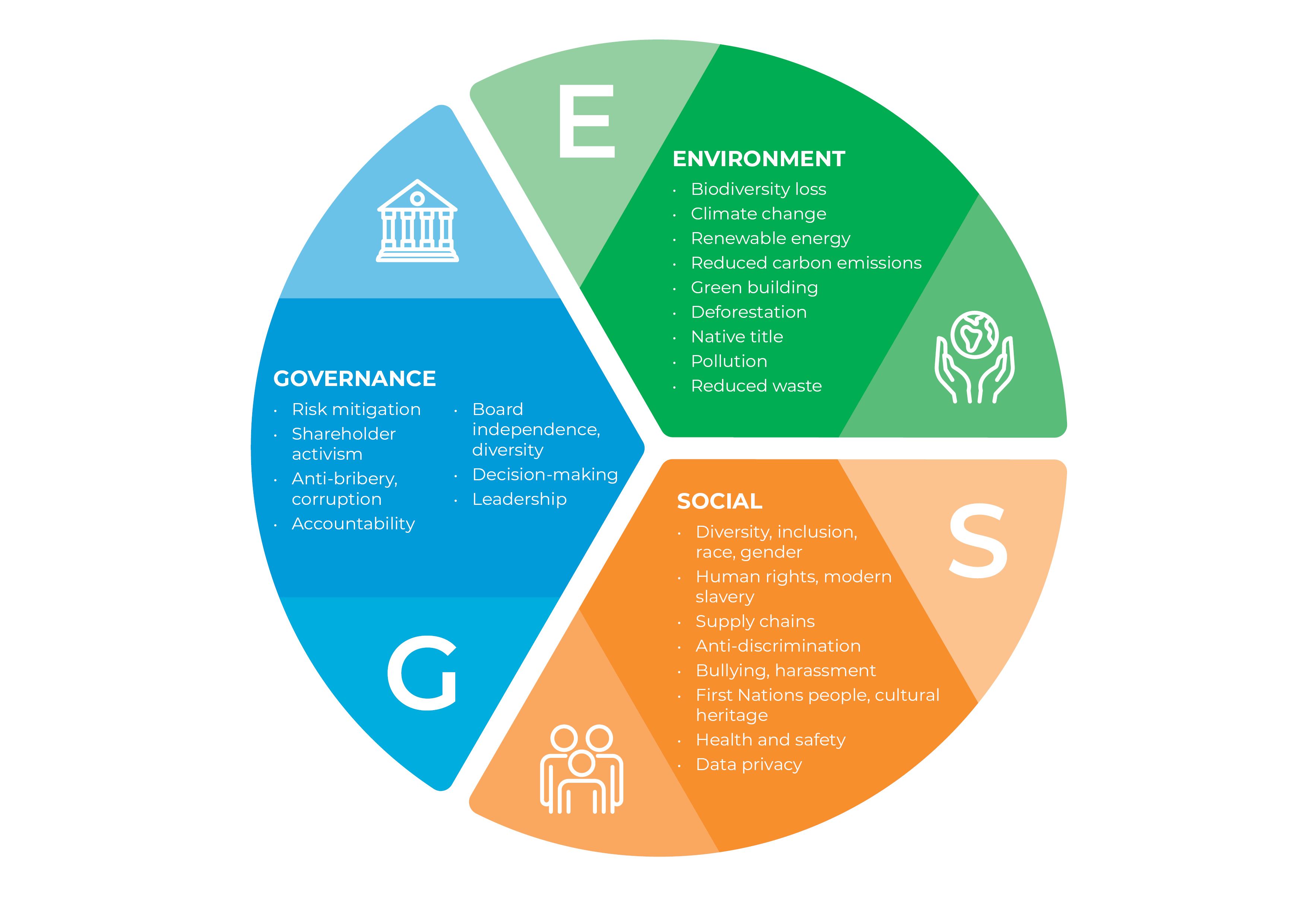

It was never clear exactly why E, S, and G were the right concepts to bring together with (apparently) equal weighting or how they were connected to each other. This awkward bundle would later prove to be a liability to the ESG movement as it went mainstream in the subsequent two decades.

These two decades also saw the rise of impact investing, with impact funds seeking to provide financing to ventures making social impact even if it meant lower-than-market returns. The “impact economy” grew alongside ESG until the lines blurred between them, so much so that many of our incoming MBA students expect that doing what is right will always be the profit-maximizing choice.

Meanwhile, within ESG circles there has been increased discussion about materiality, such as the recent U.S. SEC rule requiring companies to disclose how climate change will impact a company’s financial performance forecasts that “a reasonable investor” would factor into their decision “when determining whether to buy or sell” a particular stock. The even newer concept of “double materiality” broadens the scope to include not only financial materiality — how a company’s E, S, and G matters might impact stock prices — but also impact materiality, which refers to the impact a company’s operations and products have on its stakeholders and broader society.

This bundling of financial materiality with impact investing along with the expansion of materiality to also encompass social impact helped further muddle ESG and made it an easier target for backlash. The term became so broad as to include both strategic choices that were good for business and efforts that were good for society, though not necessarily connected to the bottom line.

The E-S-G triad and double materiality are at the heart of ESG’s current challenges. ESG encompasses too many varied factors, with some viewing it as merely good business practice to thoughtfully scan risks and opportunities, and others believing it to be an important cure to every form of corporate malfeasance. Some are convinced that ESG performance enhances profitability, while others think it erodes profitability. ESG has almost become a kind of Rorschach test, where people’s varying interpretations seem rooted in their views about capitalism itself. This confusion made it difficult to standardize how to measure ESG and easy for critics to cherry pick weak metrics and for companies to shift the goal posts to avoid accountability, as we have seen with the recent spate of companies quietly retreating from unmet emissions targets. ESG’s big tent became a big problem.

We believe that more progress will be achieved if E, S, and G were unbundled into their own separate categories. Linkages should be made when they’re merited, such as the need to recognize social justice concerns when constructing or redesigning infrastructure to decarbonize and boost the resilience of our energy and transportation systems (a link often referred to as climate justice).

The clarity of measuring many environmental factors has far outpaced social factors. For example, the world has converged on measuring greenhouse gas (GHG) emissions, and approaches to reduce them are increasingly clear. That’s one reason why BlackRock can confidently pivot to introduce “transition investing” products, which facilitate investments in companies developing technologies and products that seek to accelerate society’s transition to a less-GHG-intensive economy. There is also more consensus in the business community on the threats that climate change poses and how to measure GHG emissions than there is on the benefits of and metrics to rigorously measure social topics like diversity, equity, and inclusion.

Firms are unlikely to walk away from all of their ESG efforts and BlackRock, among other firms, retain some ESG funds. The movement has secured many victories, including the institutionalization of these factors into law such as the European Union’s historic Corporate Sustainability Reporting Directive set to go into effect this year, and laws spanning the E.U., U.K., and U.S requiring companies to engage in more due diligence of social and environmental concerns in their supply chains. As a result, many multinational companies will still need to measure and report key ESG metrics, regardless of ESG’s waning popularity in the U.S.

Many stakeholders are still demanding ESG performance. And some (including one of us) have argued that senior managers should look beyond their operations and supply chains to align those E and S strategies with another factor, “P” for politics, to integrate how their firms are using lobbying and campaign contributions to influence legislative, regulatory, and administrative actions on these E and S issues.

On the supply side, we expect firms to focus on E, S, and G topics that are measurable and material. Many will focus on the “E” domain where the term “transition investing” has not yet evoked much pushback, and where firms’ efforts to bolster their climate resilience are somewhat less controversial. This concept includes efforts to manage companies’ risks related to the consequences of climate change, from heat to cold snaps and droughts to floods, on operations, employees, supply chains, and customers. “G” will likely be subsumed back into the broader accounting and regulatory framework, which has been influenced by the ESG movement quite significantly over the last 20 years.

“S” is the most contested, where we see major cultural divides, including along geographic and demographic dimensions, over the value of diversity. In the U.S., for example, the Supreme Court’s recent ruling limiting affirmative action in university admissions decisions is already affecting corporate practices. Other “S” topics like toxic products, worker safety, and community impact will probably continue to be framed as a “bad apples” problem, where serious scrutiny is concentrated on only a few large firms while most others will check the boxes on various employee engagement efforts and appear on at least one of the many lists of top corporate citizens.

ESG is at an inflection point. Like a long list of ancestral acronyms, including CSR and SRI, it has come to represent a broad and inchoate aspiration for what business should be doing beyond maximizing shareholder value. These ideals have sometimes been pitched as win-wins that will increase profits, and at other times as advocating that companies engage in tradeoffs to generate positive but below-market returns in order to improve their social impact.

With ESG advocates on the defensive, business leaders need a new roadmap to determine which factors to incorporate into their business strategies and operations — and their political advocacy — and how they will communicate this to their stakeholders.

Corporate leaders, including those not bound by the emerging sustainability reporting and due diligence legal requirements, should adopt a two-pronged approach. First, identify the sustainability issues that have the most potential impact on the bottom line — analogous to the concept of financial materiality — and solve for them. This requires scanning for the biggest opportunities and threats that environmental and social issues pose to a company’s short- and long-term competitiveness.

As Bob Eccles has noted, this requires a clear statement of purpose and priorities along with an acknowledgment that firms will have to make difficult trade-offs between important financial and social priorities.

The second part of the approach is to identify the most material negative impacts your firm is having on society, and invest serious resources to developing practical solutions, which often entails working with other companies and nonprofits and advocating for changes to government policies to develop systemic solutions. This too is important for a company’s long-term competitiveness.

If we have indeed reached peak ESG, firms that can do these two things at once will be the leaders of managing business and society issues in this new era.

Half the price, all the fun. Get 50% OFF any Paramount+ annual plan for a limited time! Take advantage of the fall offer and start streaming...

CLICK HERE FOR SPECIAL DISCOUNT LINK

Everyday your story is being told by someone. Who is telling your story? Who are you telling your story to?

Email your sustainable story ideas, professional press releases or podcast submissions to thecontentcreationstudios(AT)gmail(DOT)com.